HMDA and Housing Demand

The Home Mortgage Disclosure Act (HMDA) provides detailed information on mortgage lending activity, offering valuable insight into housing demand. Data on the number of loan applications can indicate whether housing demand is strong or weak, while approval rates reflect individuals' and families' ability to secure financing. Additional information, such as interest rates, income distribution, and property values, can paint a picture of the local economy.

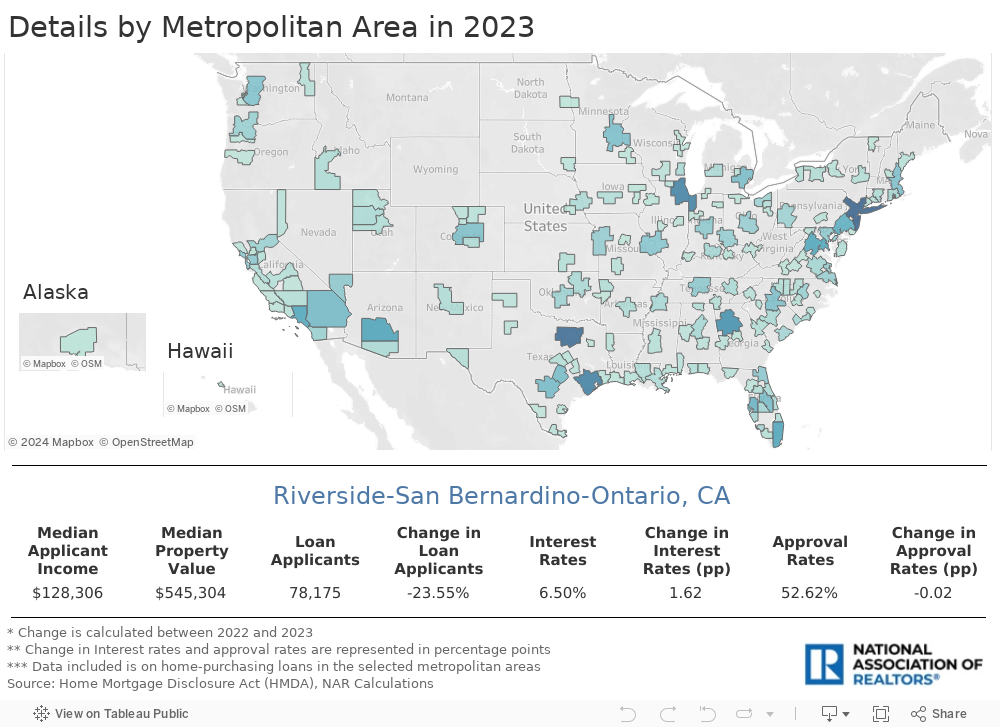

Let’s look at the most recent data from HMDA, which highlights changes in housing demand in U.S. metropolitan areas between 2022 and 2023. Nationwide, the number of home-purchase loan applications has declined from 7.9 million to 6.5 million. As a result, 3.5 million home-purchase loans were originated in 2023, compared to 4.4 million in 2022. The average interest rate on mortgages has increased from 4.96% in 2022 to 6.56% in 2023, while the median loan amount has decreased from $290,762 to $288,365, and the median property value has decreased from $354,953 to $353,957 respectively.

Since all real estate is local, this analysis will focus on home-purchasing loans in 175 of the country's largest metropolitan areas.

Loan Applications

In December 2023, mortgage interest rates fell to their lowest level in six months, averaging 6.82%. Nevertheless, the combination of relatively high interest rates and elevated property values continued to price out many potential buyers from the market, resulting in fewer loan applications. The U.S. lost 1.3 million home-purchase loan applicants between 2022 and 2023, leading to over 900,000 fewer loan originations in 2023.

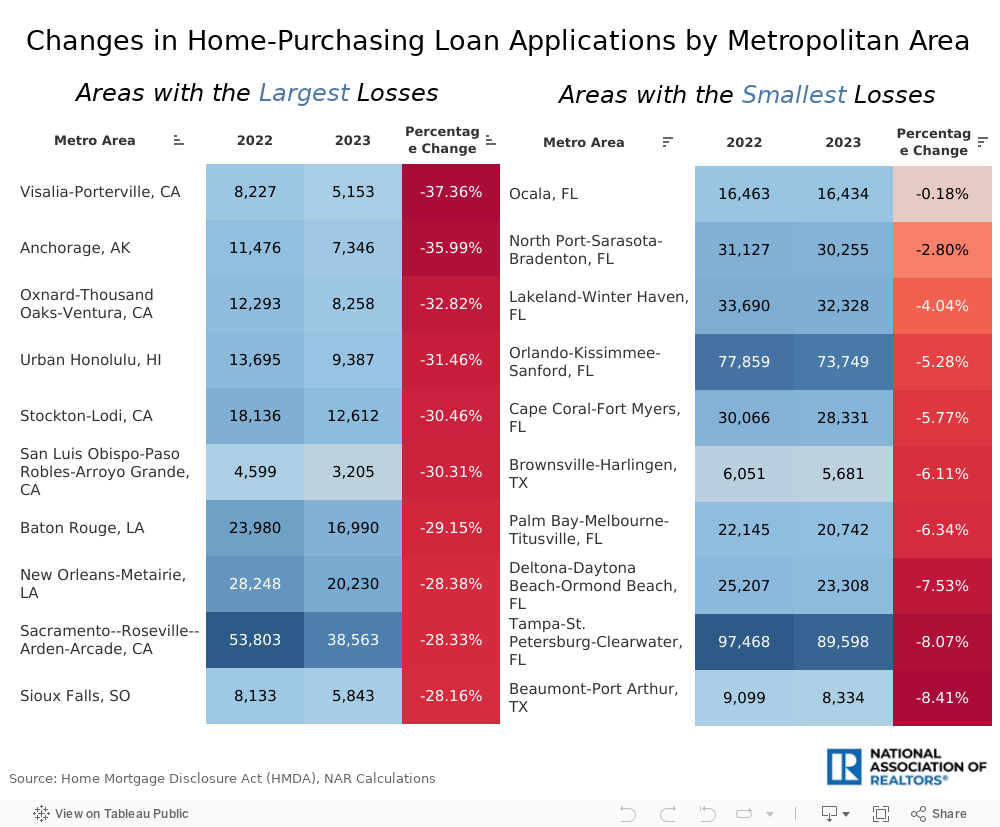

The most notable change that year was a 37.36% decline in applications in Visalia-Porterville, CA, with 3,074 fewer applicants. Following Visalia-Porterville were Anchorage, AK (-35.99%), Oxnard-Thousand Oaks-Ventura, CA (-32.82%), and Urban Honolulu, HI (-31.46%). Conversely, the smallest change was 0.18% in Ocala, FL, losing 29 applications that year. Despite a 24.14% drop in applications, the New York-Newark-Jersey City, NY-NJ-PA still led with a total of 215,251 applications in 2023. Burlington, VT, had the fewest applications, with only 2,931 loan applicants.

Mortgage Interest Rates

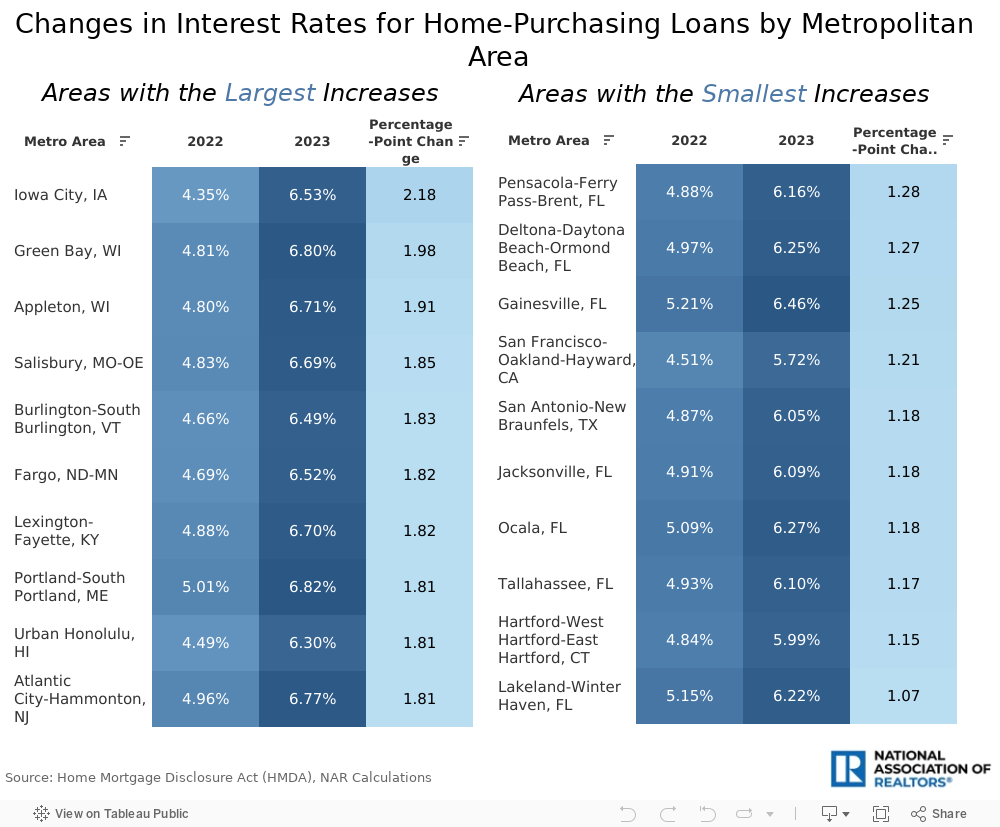

In contrast to loan applications, mortgage rates rose in all 175 metropolitan areas, increasing from an average of 4.96% in 2022 to 6.56% in 2023. Iowa City, IA, which had the lowest rate of 4.35% in 2022, experienced the largest increase, climbing by 2.18 percentage points to 6.53% in 2023. However, most areas didn’t experience such significant rate changes. For instance, Flint, MI, had the highest mortgage rate, increasing by 1.49 percentage points from an average of 5.63% in 2022 to 7.12% in 2023. In 2023, the lowest mortgage rate was 5.72% in the San Francisco-Oakland-Hayward, CA area, and the smallest change was 1.07 percentage points in Lakeland-Winter Haven, FL.

Approval Rates

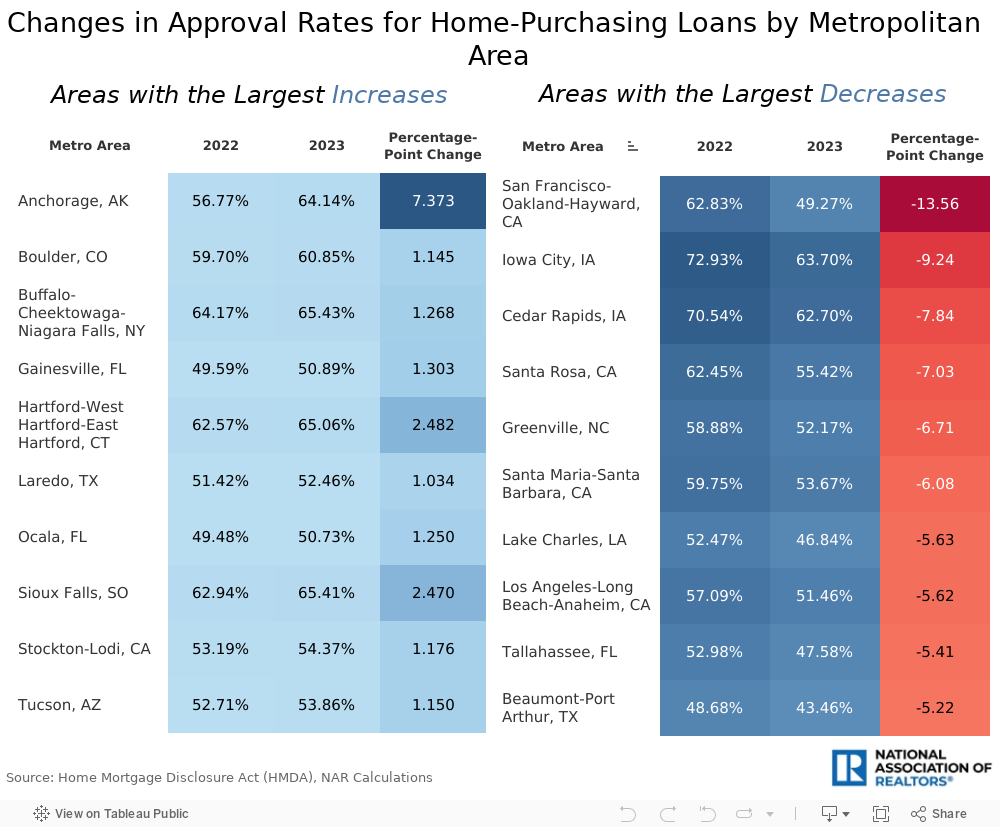

NAR calculates the loan approval rate as the ratio between loans originated and the total number of applications in a metropolitan area. The national approval rate for home-purchasing loans was 55.1% in 2022 and 52.7% in 2023. The state of Wisconsin led in loan approvals, with two of its metropolitan areas having the highest approval rates for both 2022 and 2023: Green Bay, where 76.8% of the loans were approved in 2022, and Appleton, where 75.44% of the loans were approved in 2023. In comparison, the lowest approval rates were recorded in two metropolitan areas in Texas: McAllen-Edinburg-Mission, where only 44.43% of the applications were approved in 2022, and Beaumont-Port Arthur, where only 43.46% were approved in 2023.

Between 2022 and 2023, only 27 metropolitan areas had an increase in the rate of approvals. The largest increase was 7.37 percentage points in Anchorage, AK, while the smallest was 0.08 percentage points in Washington-Arlington-Alexandria, DC-VA-MD-WV. Conversely, the largest decrease was -13.56 in San Francisco-Oakland-Hayward, CA, and the smallest was -0.06 points in Rochester, NY.

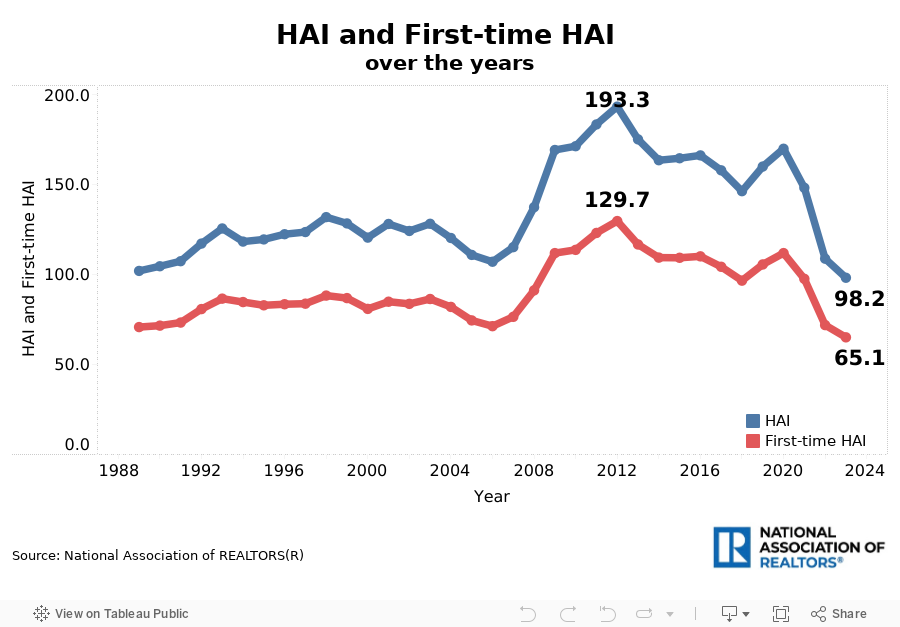

The combination of rising mortgage rates and persistently increasing property values has been reducing affordability, making it difficult for many potential buyers, especially first-time home buyers, to enter the market in recent years. However, there is some optimism for the near future: If mortgage rates remain below 7%, we may see an increase in loan applications and approval rates in 2024.

The Home Mortgage Disclosure Act (HMDA) provides detailed information on mortgage lending activity, offering valuable insight into housing demand. Data on the number of loan applications can indicate whether housing demand is strong or weak, while approval rates reflect individuals' and families' ability to secure financing. Additional information, such as interest rates, income distribution, and property values, can paint a picture of the local economy.

Let’s look at the most recent data from HMDA, which highlights changes in housing demand in U.S. metropolitan areas between 2022 and 2023. Nationwide, the number of home-purchase loan applications has declined from 7.9 million to 6.5 million. As a result, 3.5 million home-purchase loans were originated in 2023, compared to 4.4 million in 2022. The average interest rate on mortgages has increased from 4.96% in 2022 to 6.56% in 2023, while the median loan amount has decreased from $290,762 to $288,365, and the median property value has decreased from $354,953 to $353,957 respectively.

Since all real estate is local, this analysis will focus on home-purchasing loans in 175 of the country's largest metropolitan areas.

Loan Applications

In December 2023, mortgage interest rates fell to their lowest level in six months, averaging 6.82%. Nevertheless, the combination of relatively high interest rates and elevated property values continued to price out many potential buyers from the market, resulting in fewer loan applications. The U.S. lost 1.3 million home-purchase loan applicants between 2022 and 2023, leading to over 900,000 fewer loan originations in 2023.

The most notable change that year was a 37.36% decline in applications in Visalia-Porterville, CA, with 3,074 fewer applicants. Following Visalia-Porterville were Anchorage, AK (-35.99%), Oxnard-Thousand Oaks-Ventura, CA (-32.82%), and Urban Honolulu, HI (-31.46%). Conversely, the smallest change was 0.18% in Ocala, FL, losing 29 applications that year. Despite a 24.14% drop in applications, the New York-Newark-Jersey City, NY-NJ-PA still led with a total of 215,251 applications in 2023. Burlington, VT, had the fewest applications, with only 2,931 loan applicants.

Mortgage Interest Rates

In contrast to loan applications, mortgage rates rose in all 175 metropolitan areas, increasing from an average of 4.96% in 2022 to 6.56% in 2023. Iowa City, IA, which had the lowest rate of 4.35% in 2022, experienced the largest increase, climbing by 2.18 percentage points to 6.53% in 2023. However, most areas didn’t experience such significant rate changes. For instance, Flint, MI, had the highest mortgage rate, increasing by 1.49 percentage points from an average of 5.63% in 2022 to 7.12% in 2023. In 2023, the lowest mortgage rate was 5.72% in the San Francisco-Oakland-Hayward, CA area, and the smallest change was 1.07 percentage points in Lakeland-Winter Haven, FL.

Approval Rates

NAR calculates the loan approval rate as the ratio between loans originated and the total number of applications in a metropolitan area. The national approval rate for home-purchasing loans was 55.1% in 2022 and 52.7% in 2023. The state of Wisconsin led in loan approvals, with two of its metropolitan areas having the highest approval rates for both 2022 and 2023: Green Bay, where 76.8% of the loans were approved in 2022, and Appleton, where 75.44% of the loans were approved in 2023. In comparison, the lowest approval rates were recorded in two metropolitan areas in Texas: McAllen-Edinburg-Mission, where only 44.43% of the applications were approved in 2022, and Beaumont-Port Arthur, where only 43.46% were approved in 2023.

Between 2022 and 2023, only 27 metropolitan areas had an increase in the rate of approvals. The largest increase was 7.37 percentage points in Anchorage, AK, while the smallest was 0.08 percentage points in Washington-Arlington-Alexandria, DC-VA-MD-WV. Conversely, the largest decrease was -13.56 in San Francisco-Oakland-Hayward, CA, and the smallest was -0.06 points in Rochester, NY.

The combination of rising mortgage rates and persistently increasing property values has been reducing affordability, making it difficult for many potential buyers, especially first-time home buyers, to enter the market in recent years. However, there is some optimism for the near future: If mortgage rates remain below 7%, we may see an increase in loan applications and approval rates in 2024.

Categories

Recent Posts

5966 Fairview Rd, Suite 400, Charlotte, NC 28210, United States